How to Avoid Junk Dealer Fees in 2026

Which fees on a car dealer's worksheet are real, which are pure profit, and the exact scripts to push back in the F&I office without blowing the deal.

The sticker price is not the price you pay. By the time you're in the F&I office, dealers have typically added $800–$3,000 in fees on top of the agreed vehicle price. Some are legitimate. Most are negotiable or pure profit. Here's how to tell the difference.

Always ask for the out-the-door price first

Before you agree to anything, ask: "What's the out-the-door price, including all fees, taxes, and registration?" Write it down. A dealer who won't give you this number in writing before you sit in the finance office is using the separate-line-item format to obscure the total.

Taxes and government fees are non-negotiable. Everything else is.

The fee breakdown

Real fees you'll pay everywhere

Documentation fee (doc fee) This is the dealer's charge for preparing the title, sales contract, and related paperwork. It's real, and in many states it's capped by law:

| State | Doc fee cap |

|---|---|

| California | $85 |

| New York | Negotiable (typically $75–$200) |

| Texas | class="relative z-10"50 |

| Florida | Uncapped (typically $500–$900) |

| Ohio | $250 |

| Illinois | $324.24 |

In uncapped states, doc fees routinely hit $700–$900. You can try to negotiate it down. They won't always move on it, but asking costs nothing.

Title and registration fees Set by your state's DMV. Non-negotiable. These go to the government, not the dealer.

Sales tax Set by your state and sometimes your county. Non-negotiable.

Negotiable but sometimes legitimate

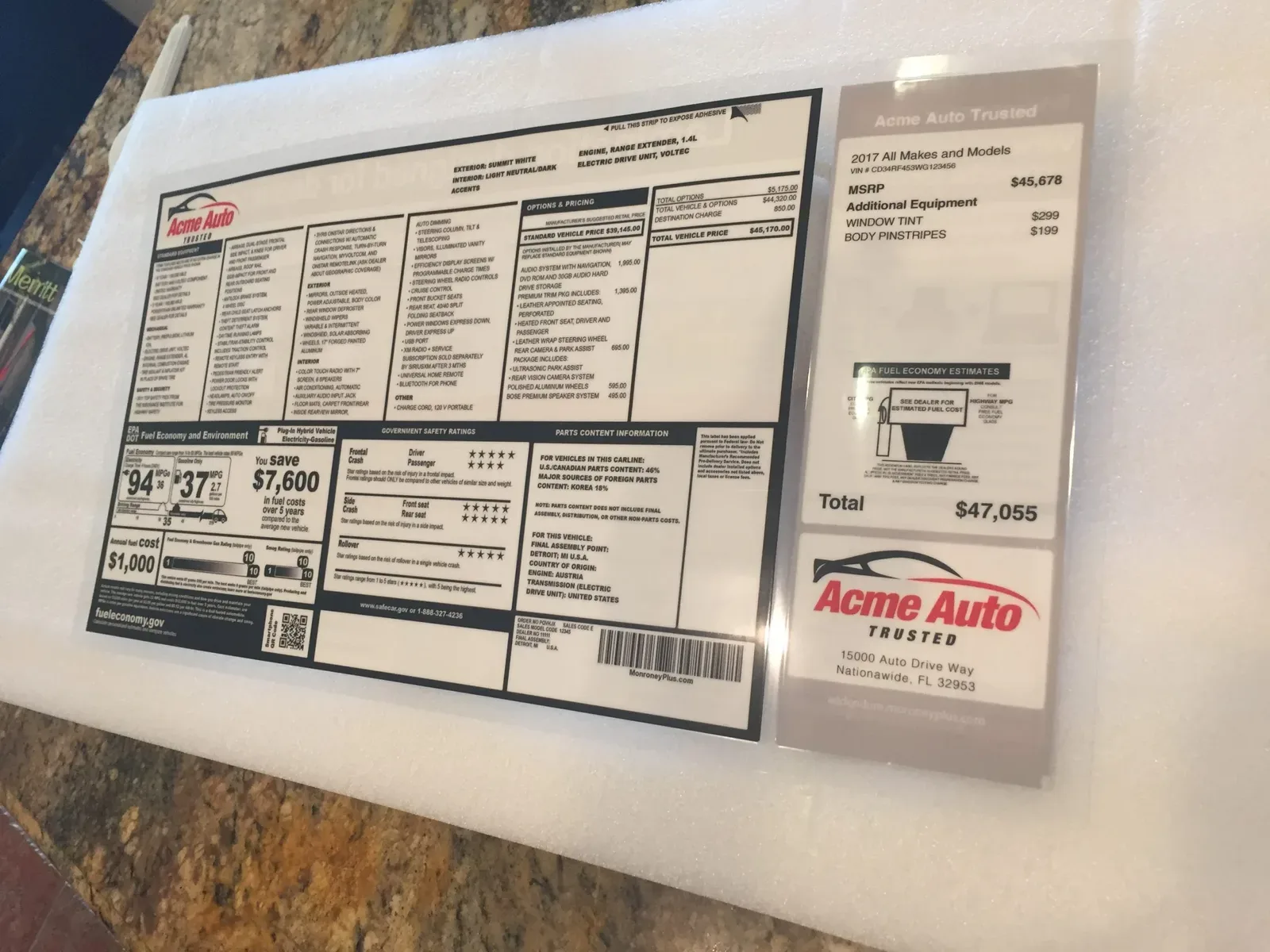

Dealer prep fee / reconditioning fee For new cars, this is almost always junk. The manufacturer pays the dealer to prep the vehicle for sale. You're being charged twice. For used vehicles, there may be a genuine reconditioning cost, but it should be reflected in the asking price, not added as a line item.

Market adjustment / market value adjustment This is extra profit disguised as a fee, applied when a vehicle is in short supply. If you're seeing a market adjustment on a vehicle that isn't actually in short supply, push back hard. On truly allocated models (some trucks, some performance cars), you may have less leverage. On mainstream inventory, refuse it.

Junk fees: refuse these

Nitrogen tire inflation Air is 78% nitrogen. You are paying $200–$400 for someone to put air in your tires and hand you a receipt. Decline.

Paint protection / paint sealant / ceramic coating The F&I office will quote this at $400– class="relative z-10",200. The product applied is typically a $20 bottle of sealant applied by a detailer for 10 minutes. If you want ceramic coating, have it applied by an independent shop for $300–$600 with an actual warranty.

Fabric protection / interior protection See above. Scotchgard is class="relative z-10"0 at any hardware store.

VIN etching / window etching Marketed as theft deterrence. The research on its effectiveness as a theft deterrent is mixed at best. Often pre-installed by the dealer before you arrive, presented as non-removable. You can decline to pay for it even if it's already on the car.

LoJack / GPS tracking device If you want a GPS tracker for your car, aftermarket options exist for class="relative z-10"00–$200 with annual subscription. Dealer-installed versions at $500–$800 are the same category.

Key replacement insurance / tire-and-wheel protection / dent protection Bundled products with exclusion-heavy contracts. Read the exclusions before buying any of them.

How to handle the F&I office

The finance office is a profit center. The finance manager's job is to increase the back-end gross on your deal. That's not cynicism, it's their compensation structure. Knowing that reframes the conversation.

Script for new fees that appear on the worksheet:

"This wasn't in the price we agreed on in the showroom. I want to honor the deal we made. Can you remove this and confirm the out-the-door total we discussed?"

Script for add-on products:

"I'm not interested in any add-on products. I want to keep this straightforward. Can we go straight to the contract signing?"

If they tell you a fee is "required" or "mandatory," ask to see that in writing from the manufacturer. With the exception of legitimate government fees and the doc fee, nothing is mandatory.

The credit score angle. Some F&I managers will tell buyers with fair credit that purchasing products will improve their loan approval odds. This is false. The loan is already approved before you sit down in the finance office.

The final worksheet check

Before you sign anything, add up the numbers yourself. Price + tax + title + registration + doc fee = out-the-door. Every other line is either something you agreed to or something you didn't. Cross out what you didn't agree to and initial it. The deal doesn't have to close that night.

For a broader look at the entire purchase process, the negotiation guide covers the full workflow from first contact to final signature.

From the Buying Guide

Related articles

How to Negotiate a New Car in 2026: A Step-by-Step Guide

A no-BS walkthrough on how to negotiate your next new car purchase — pricing research, dealer tactics to avoid, financing, and the exact scripts that work.

How to Read a New-Car Window Sticker in 2026

A line-by-line guide to the Monroney label. What every number means, where dealers add markup, and how to use the sticker as your negotiation tool.

Your Lease Is Ending: Buy It, Return It, or Trade It?

The 90-day lease-end playbook: how to check for equity, when the buyout beats returning, disposition and wear charges, and the exact steps in order.